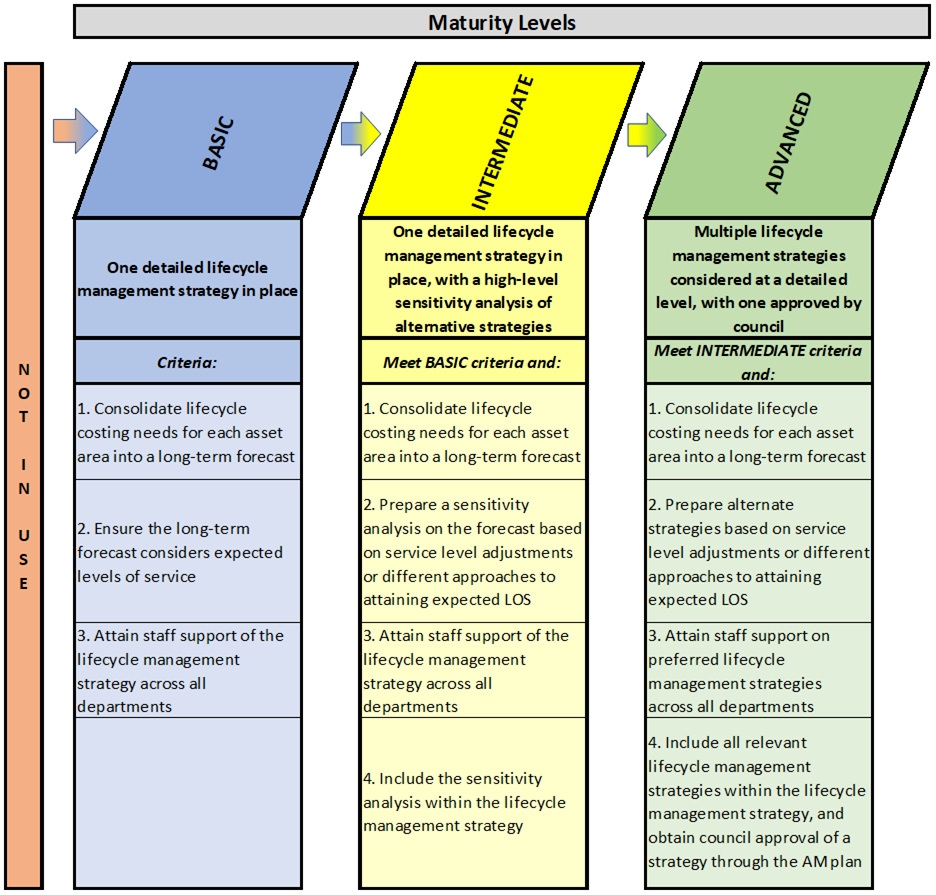

This framework is intended for municipalities of all sizes

and maturity levels. The use of the maturity diagrams within this framework can

help municipalities identify their current levels of maturity for each AM area.

In addition, the diagrams provide possible approaches for municipalities to

undertake in order to move to a higher level of maturity over time. Adaptations

of the following diagram are used throughout this document to summarize

maturity levels according to the themes and questions explored in each chapter:

Municipalities that are not undertaking the components

described in a particular section of this framework should focus on meeting the

basic level requirements outlined in the maturity level diagram.

At the basic level of maturity, a municipality is

undertaking the components of asset management shown in blue and will take

steps to advance their asset management by implementing the components

described under the intermediate level heading.

At the intermediate level of maturity, a municipality

is currently meeting the requirements shown in yellow and to advance their

asset management will take steps to implement the components described under

the advanced level heading.

At the advanced level of maturity, a municipality is

currently meeting the requirements shown in green.

These maturity framework visuals are found throughout this

document. Preceding all maturity level diagrams is a self-assessment question

for the reader to consider to help determine where their municipality best fits

within the framework.

5.2

Overview

The Ontario “Building Together Guide for Municipal Asset

Management Plans” defines an asset management strategy as:

The set of planned actions that will enable the

assets to provide the desired levels of service in a sustainable way, while

managing risk, at the lowest lifecycle cost.

Moving forward, the “asset management strategy” will be

referred to as the “lifecycle management strategy”, which provides a more

accurate description of the requirements in this section. The actions defined

and identified within the lifecycle management strategy detail how assets

should be maintained, renewed/rehabilitated, replaced, disposed, or expanded

upon. All strategies considered will attempt to move the municipality towards

expected levels of service in an efficient and effective manner.

Lifecycle Costing

Lifecycle costing is defined by IIMM as:

The total cost of an asset throughout its life

including planning, design, construction, acquisition, operation, maintenance,

rehabilitation and disposal costs.

Within this is the true challenge of public infrastructure

management which is:

To ensure that the assets we have now and those

that will be created in the future provide suitable levels of service at a cost

the community can afford.

Lifecycle costing is comprised of the following costs over

an asset’s useful life:

·

Acquisition or construction;

·

Operating;

·

Maintaining;

·

Rehabilitating;

·

Replacing;

·

Disposing; and

·

Non-infrastructure solutions.

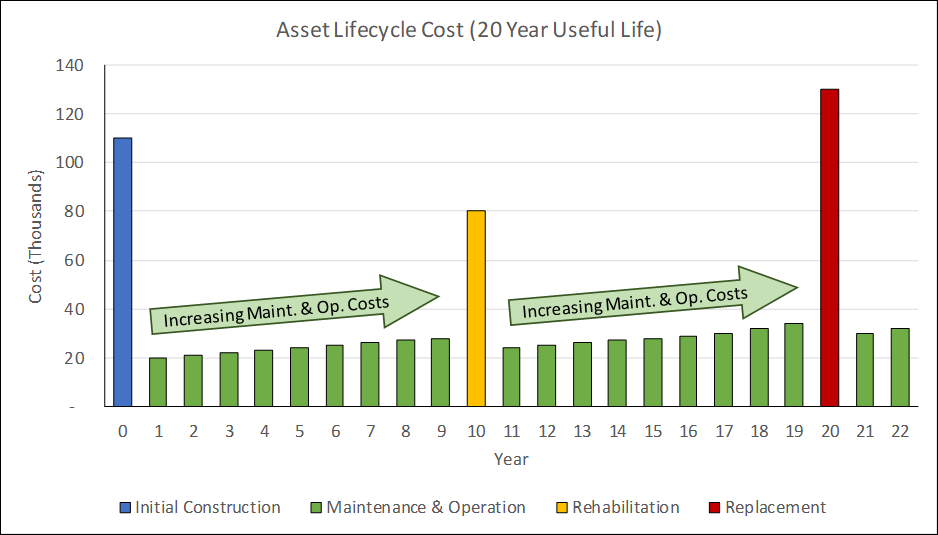

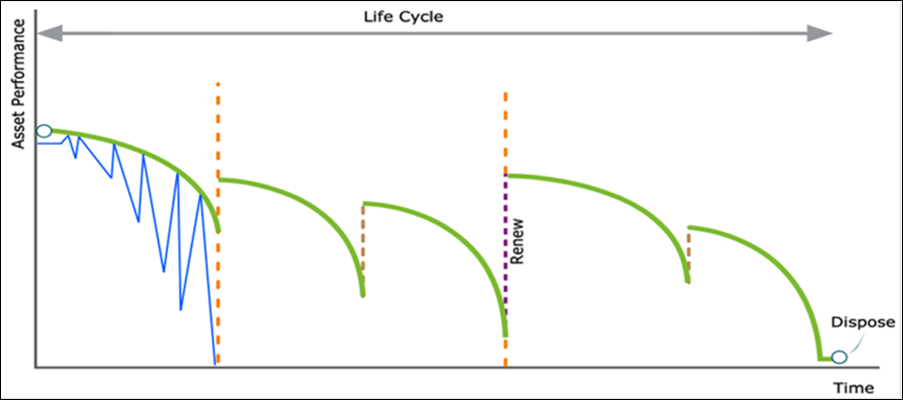

All of the cost elements above should be considered when

determining the true cost of an asset over its useful life. The resulting cost

profile may look something like the following figure.

Figure 5‑1

Sample Asset Cost Profile

Figure 5-1 (above) illustrates:

·

Initial construction of the asset occurs in year 0;

·

Maintenance and operational costs are incurred annually,

increasing as the asset deteriorates (from year 1 to 9);

·

Rehabilitation of the asset is shown in year 10, which has the

result of extending the remaining useful life of the asset and reducing annual

maintenance and operational costs;

·

Maintenance and operational costs are incurred annually,

increasing as the asset deteriorates (from year 11 to 19);

·

Complete asset replacement occurs in year 20; and

·

Annual maintenance and operational costs continue forward on the

new asset.

Asset managers strive to achieve the lowest lifecycle cost

for all assets. The example described above provides an indication of the total

lifecycle cost by summing all annual costs over the asset’s life. Comparing

alternative lifecycle scenarios, such as alternative interventions and

frequencies, allows municipalities to experiment with the impact of differing

lifecycle forecasts on the assets themselves and the services being provided.

This methodology will be expanded upon further in later sections within this

chapter.

Infrastructure for Jobs and Prosperity (IJPA) Act and O.

Reg 588/17 Requirements

O.Reg 588/17 outlines the

following requirements with respect to the Lifecycle Management Strategy:

Every municipality shall prepare an asset management plan in

respect of its core municipal infrastructure assets by July 1, 2021, and

in respect of all of its other municipal infrastructure assets by July 1,

2023.

A municipality’s AM plan must

include the following (for each asset category):

a) The lifecycle

activities that would need to be undertaken to maintain the current levels of

service for each of the 10 years following the year for which the current

levels of service are determined and the costs of providing those activities

based on an assessment of the following:

i.

The full lifecycle of the assets.

ii.

The options for which lifecycle activities could potentially be

undertaken to maintain the current levels of service.

iii.

The risks associated with the options referred to in subparagraph ii.

iv.

The lifecycle activities referred to in subparagraph ii that can be

undertaken for the lowest cost to maintain the current levels of service.

b) For

municipalities with a population of less than 25,000, as reported by Statistics

Canada in the most recent official census, the following:

i.

A description of assumptions regarding future changes in population or

economic activity.

ii.

How the assumptions referred to in subparagraph i relate to the required

lifecycle activities described above.

c) For

municipalities with a population of 25,000 or more, as reported by Statistics

Canada in the most recent official census, the following:

i.

With respect to municipalities in the Greater Golden Horseshoe growth

plan area, if the population and employment forecasts for the municipality are

set out in Schedule 3 or 7 to the 2017 Growth Plan, those forecasts.

ii.

With respect to lower-tier municipalities in the Greater Golden

Horseshoe growth plan area, if the population and employment forecasts for the

municipality are not set out in Schedule 7 to the 2017 Growth Plan, the portion

of the forecasts allocated to the lower-tier municipality in the official plan

of the upper-tier municipality of which it is a part.

iii.

With respect to upper-tier municipalities or single-tier municipalities

outside of the Greater Golden Horseshoe growth plan area, the population and

employment forecasts for the municipality that are set out in its official

plan.

iv.

With respect to lower-tier municipalities outside of the Greater Golden

Horseshoe growth plan area, the population and employment forecasts for the

lower-tier municipality that are set out in the official plan of the upper-tier

municipality of which it is a part.

v.

If, with respect to any municipality referred to in subparagraph iii or

iv, the population and employment forecasts for the municipality cannot be

determined as set out in those subparagraphs, a description of assumptions

regarding future changes in population or economic activity.

vi.

For each of the 10 years following the year for which the current levels

of service are determined, the estimated capital expenditures and significant

operating costs related to the lifecycle activities required to maintain the

current levels of service in order to accommodate projected increases in demand

caused by growth, including estimated capital expenditures and significant

operating costs related to new construction or to upgrading of existing

municipal infrastructure assets.

By July 1, 2024, every asset

management plan must include the following additional information:

a) A lifecycle

management and financial strategy that sets out the following information with

respect to the assets in each asset category for the 10-year period:

i.

An identification of the lifecycle activities that would need to be

undertaken to provide the proposed levels of service described in paragraph 1,

based on an assessment of the following:

A.

The full lifecycle of the assets.

B.

The options for which lifecycle activities could potentially be

undertaken to achieve the proposed levels of service.

C.

The risks associated with the options referred to in sub-subparagraph B.

D.

The lifecycle activities referred to in sub-subparagraph B that can be

undertaken for the lowest cost to achieve the proposed levels of service.

ii.

An estimate of the annual costs for each of the 10 years of undertaking

the lifecycle activities identified in subparagraph i, separated into capital

expenditures and significant operating costs.

iii.

An identification of the annual funding projected to be available to

undertake lifecycle activities and an explanation of the options examined by

the municipality to maximize the funding projected to be available.

iv.

If, based on the funding projected to be available, the municipality

identifies a funding shortfall for the lifecycle activities identified in

subparagraph i,

A.

an identification of the lifecycle activities, whether set out in

subparagraph i or otherwise, that the municipality will undertake, and

B.

if applicable, an explanation of how the municipality will manage the

risks associated with not undertaking any of the lifecycle activities identified

in subparagraph i.

b) For

municipalities with a population of less than 25,000, as reported by Statistics

Canada in the most recent official census, a discussion of how the assumptions

regarding future changes in population and economic activity informed the

preparation of the lifecycle management and financial strategy.

c) For

municipalities with a population of 25,000 or more, as reported by Statistics

Canada in the most recent official census,

i.

the estimated capital expenditures and significant operating costs to

achieve the proposed levels of service as described in paragraph 1 in order to

accommodate projected increases in demand caused by population and employment

growth, as set out in the forecasts or assumptions referred to in paragraph 6

of subsection 5 (2), including estimated capital expenditures and significant

operating costs related to new construction or to upgrading of existing

municipal infrastructure assets,

ii.

the funding projected to be available, by source, as a result of

increased population and economic activity, and

iii.

an overview of the risks associated with implementation of the asset

management plan and any actions that would be proposed in response to those

risks.

To what extent are non-infrastructure solutions incorporated

into the lifecycle management strategy?

Background

Cost reduction is a consistent driver across most

municipalities, and the same is true for asset management. Investment in municipal

assets is subject to limited funding, so if the same outcome can be produced at

a lower cost, more can be done with the funding that is available. At the same

time, care must be taken to ensure that a cost reduction today does not result

in a cost escalation in the future.

Non-infrastructure solutions are actions or policies that

are not capital in nature, which result in the lowering of costs and/or extend

the useful life of an asset.

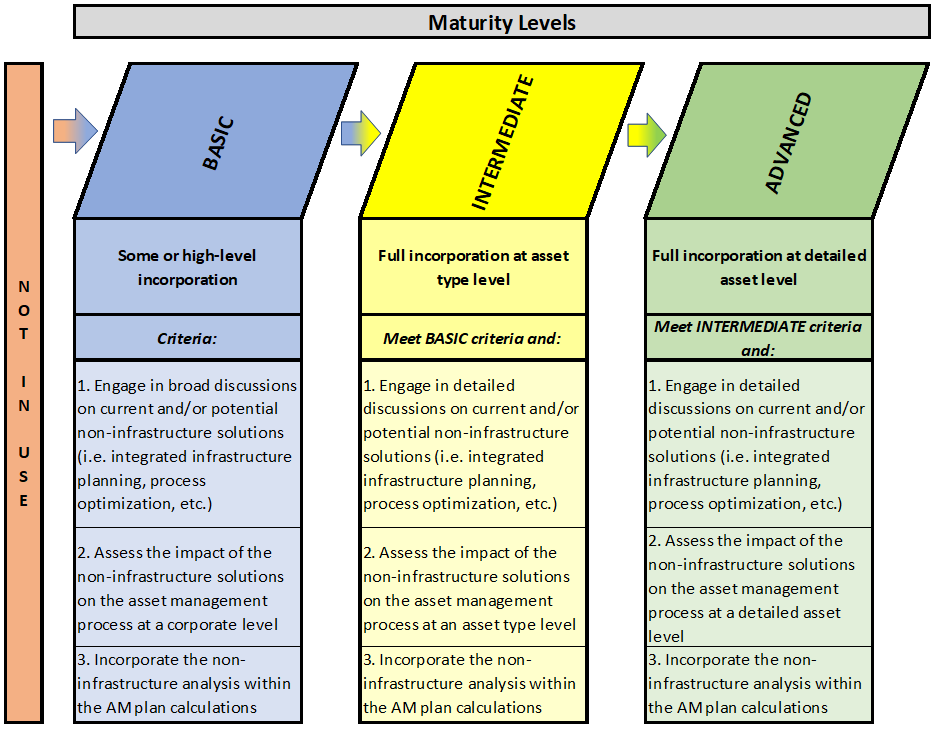

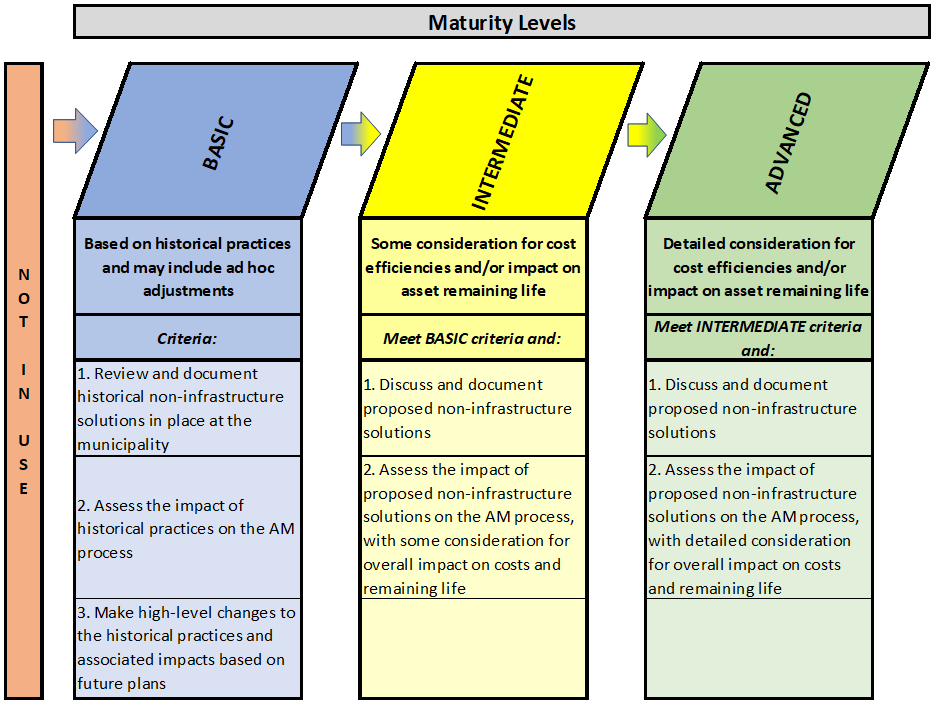

Levels of Maturity

To what extent are non-infrastructure solutions

incorporated into the lifecycle management strategy?

At the basic level of maturity, non-infrastructure

solutions are incorporated into the lifecycle management strategy to some

extent. Municipalities may engage in broad discussions on current and/or

potential non-infrastructure solutions. The impact of these solutions on the

asset management process would be assessed at a corporate level. Finally, the

non-infrastructure analysis are incorporated within the asset management plan

calculations.

At the intermediate level of maturity,

non-infrastructure solutions are incorporated fully into the lifecycle

management strategy at the asset level. Municipalities may engage in detailed

discussions on current and/or potential non-infrastructure solutions. The

impact of these solutions on the asset management process is assessed at an

asset level. Finally, the non-infrastructure analysis is incorporated within

the asset management plan calculations.

At the advanced level of maturity, non-infrastructure

solutions are incorporated fully into the lifecycle management strategy at a

detailed asset level. Municipalities may engage in detailed discussions on

current and/or potential non-infrastructure solutions. The impact of these

solutions on the asset management process is assessed at a detailed asset

level. Finally, the non-infrastructure analysis is incorporated within the

asset management plan calculations.

Non-Infrastructure

Solutions Introduction

Non-infrastructure solutions include policies, processes, or

strategies that:

·

Reduce asset related costs (i.e. operating, maintaining,

rehabilitation, replacement, expansion); and/or

·

Improve asset performance (resulting in lower costs and/or

extended life).

Achieving cost reduction can come down to effective and

efficient non-infrastructure solutions for asset management:

·

Effectiveness involves “doing what should be done”, in terms of

policies, processes, or strategies. This can come from best practices,

legislation, or direction provided by policy, process, or strategy.

·

Efficiency involves utilizing the policies, processes, and

strategies in the best possible way.

Examples of non-infrastructure solutions

include:

Table 5‑1

Sample Non-Infrastructure Solutions

|

Solution

|

Example

|

|

Integrated Infrastructure Planning

|

Layering road, water, wastewater, and stormwater capital

forecasts together. This ensures newly paved roads don’t have to be dug up

for main replacements.

|

|

Land Use Planning

|

Manage the development of land within the municipality, ensuring

an efficient use of land and the efficient construction of assets.

|

|

Demand Management

|

Manage and forecast the demand for services within

the municipality (e.g. introduce HOV lanes, offer discounts for using

facilities at non-peak hours, etc.).

Prepare a Development Charge Background Study to manage growth.

|

|

Insurance

|

Minimize unforeseen and uncontrollable asset costs through the use

of insurance policies.

|

|

Process Optimization

|

Optimization of asset management related processes,

such as “levels of service impacts” and “determining a capital forecast”.

Optimizing these processes not only minimizes the time and resources required

to complete them, but also generates more accurate and “real time” results.

Undertake Water/Wastewater/Storm Rate Study.

|

|

Managed Failures

|

Use of asset condition, risk assessments, and levels of service to

manage and plan for where assets are “allowed” to fail, allowing available

funds to be used in more critical areas.

|

|

Procurement Policies

|

Streamline purchasing policies/by-law to increase the receipt of

competitive bids for asset purchase or construction, including the ability to

tender for “build/own/operate” agreements or “public private partnerships”.

Streamlined purchasing policies assists municipalities in getting more for

the funding that is available (i.e. pave 5 km of roads per year rather than 4

km, for the same price, given the competitive bid environment).

|

Non-infrastructure solutions can

be implemented at a high (corporate) level, at the asset type level, or at the

detailed asset level. The level at which the solutions are implemented depends

on the municipality’s level of asset management maturity as well as the type of

solution being implemented. Examples of non-infrastructure solutions are shown

in Table 5-2 (below):

Table 5‑2

Non-Infrastructure Solutions Implementation

Levels

|

Maturity Level

|

Implementation Level

|

Non-Infrastructure Solution Example

|

|

Basic

|

Corporate

(High Level)

|

Strategic Plan (asset management section), outlining corporate

mission, goals, and action items from an asset management perspective.

|

|

Intermediate

|

Asset Type Level

|

Setting an enhanced procurement policy specifically for

roads-related projects.

|

|

Advanced

|

Detailed Asset Level

|

Asset Condition/Needs Study outlining specific actions by detailed

asset, asset segment, or asset component.

|

What method is used to incorporate non-infrastructure

solutions into the lifecycle management strategy?

Background

Non-infrastructure solutions may be incorporated into the

lifecycle management strategy based on past historical practices or a more

forward-looking approach where consideration of cost efficiencies and/or impact

on asset remaining life is factored into the chosen solution(s).

Levels of Maturity

What method is used to incorporate non-infrastructure

solutions into the lifecycle management strategy?

At the basic level of maturity, municipalities will

review and document historical non-infrastructure solutions that are in place.

Municipalities will tend to incorporate non-infrastructure solutions into the

lifecycle management strategy based on historical practices and may include

subsequent ad hoc adjustments based on expected revisions to historical

practices. The impact of these practices on the asset management process are

assessed.

At the intermediate level of maturity, municipalities

give some consideration to the impact of non-infrastructure solutions on cost

efficiencies and/or impact on asset remaining life. Proposed non-infrastructure

solutions are discussed and documented at a staff level. The impact of these

solutions on the asset management process are assessed, with some consideration

for the overall impact on costs and remaining life.

At the advanced level of maturity, municipalities

give detailed consideration for cost efficiencies and/or impact on asset

remaining life within a comprehensive non-infrastructure solutions analysis.

Proposed non-infrastructure solutions are discussed and documented within this

analysis. The impact of these solutions on the asset management process is

assessed, with detailed consideration for the overall impact on asset-related

costs and remaining life.

Non-Infrastructure

Solutions Methodology

Section 5-3 (above) introduced non-infrastructure solutions with

the following examples:

·

Integrated infrastructure planning;

·

Land use planning;

·

Demand management;

·

Effective use of insurance;

·

Process optimization;

·

Managed asset failures; and

·

Procurement policies.

This section discusses the process and methods of incorporating

non-infrastructure solutions into the asset management planning process. There

are two impacts of non-infrastructure solutions for municipalities to consider:

1. Projecting the

cost of implementing the non-infrastructure solution; and

2. Projecting the

cost savings or extended asset life due to implementing the non-infrastructure

solution.

Table 5-3 (below) provides examples of how

non-infrastructure solutions can be summarized from cost and savings

perspectives.

From a cost perspective, many non-infrastructure solutions

will have ongoing and/or periodic costs throughout a forecast period, such as

study or staff costs to implement integrated infrastructure planning or process

optimization. If these costs are required every few years then the long-term

forecast should reflect this need.

From a savings or asset life perspective, an estimation of

the potential savings of each non-infrastructure solution is needed. This could

be a one-time savings, but it’s likely to have a more long-term impact.

Table 5‑3

Sample Non-Infrastructure Solutions – Cost/Savings

|

Non-Infrastructure Solution

|

Cost

|

Savings

|

|

Managed Asset Failures: Condition and

Risk Assessments for all Assets

|

$50,000 every 3 years

|

10-year capital forecast decreases from $50 million

(inflated) to $45 million (inflated)

Pick-up Truck useful life extended from 7 years to 10 years

|

|

Procurement Policies: Introduce

processes to increase the number of competitive bids received

|

$20,000 one-time study cost in 2018

$5,000 annual increase in advertising

|

Pave 5 km roads per year vs. 4 km per year currently

5% reduction in salt and sand contract

|

|

Process Optimization: Automate and

optimize the capital forecast, using asset management software

|

$70,000 one-time cost for implementation and training, plus

$20,000 annual software fee

|

Remaining service life (avg.) of assets increases

from 34 years to 48 years

Infrastructure gap anticipated to be eliminated in 7 fewer years

than anticipated

|

Once this costing analysis is

completed, the results can be used to inform the overall lifecycle management

strategy and be combined with other lifecycle costs anticipated over the

forecast period.

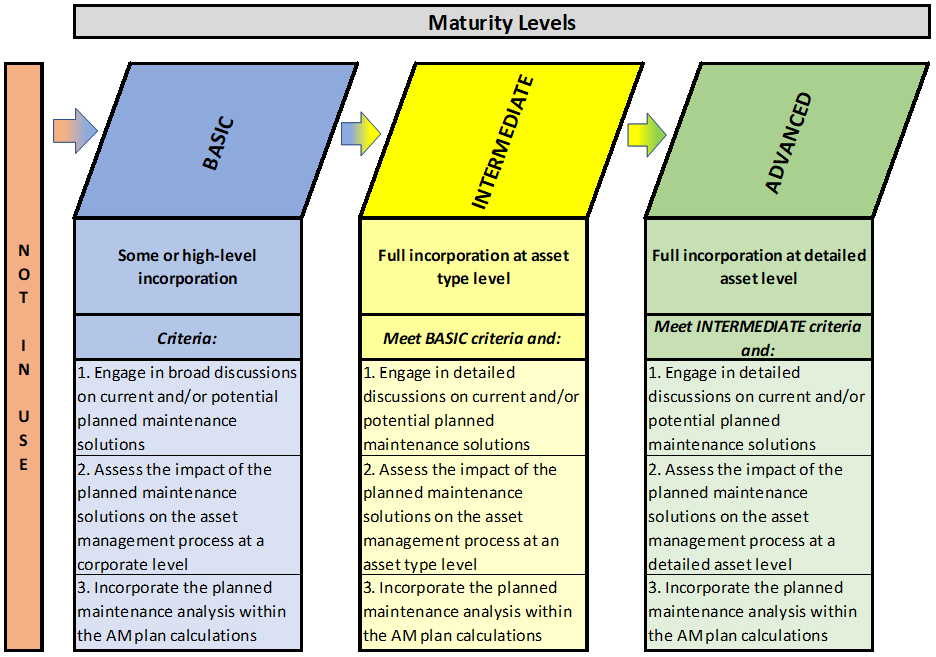

To what extent are planned maintenance solutions

incorporated into the lifecycle management strategy?

Background

Municipalities will approach planned maintenance solutions

in a number of ways. Some might base their plans on historical practices or

broad discussions at the corporate level (i.e. more high level), while others might

engage in more detailed discussions with a focus on maintenance by asset type,

or possibly at a detailed asset level.

Levels of Maturity

To what extent are planned maintenance solutions

incorporated into the lifecycle management strategy?

At the basic level of maturity, there will be some

incorporation or high-level incorporation of planned maintenance solutions into

the lifecycle management strategy. Municipalities engage in broad discussions

on current and/or potential planned maintenance solutions. The impact of these

solutions on the asset management process is assessed at a high level. Finally,

the planned maintenance analysis is incorporated within the asset management

plan calculations.

At the intermediate level of maturity, there will be

full incorporation of planned maintenance solutions into the lifecycle

management strategy by asset type. Municipalities engage in detailed

discussions on current and/or potential planned maintenance solutions at a

staff level. The impact of these solutions on the asset management process is

assessed by asset type. Finally, the planned maintenance analysis is

incorporated within the asset management plan calculations.

At the advanced level of maturity, there will be full

incorporation of planned maintenance solutions into the lifecycle management

strategy at a detailed asset level. Municipalities engage in detailed

discussions on current and planned maintenance solutions over a long-term

forecast period. The impact of these solutions on the asset management process is

assessed at a detailed asset level. Finally, the planned maintenance analysis is

incorporated within the asset management plan calculations.

Maintenance vs.

Rehabilitation

Maintenance solutions from an asset management perspective

includes regularly scheduled costs to inspect or maintain assets, or in some

cases, one-time repair costs that don’t meet the definition of

capital/rehabilitation. Section 3150 of the PSAB handbook provides an approach

to identify repairs and maintenance versus rehabilitation or “betterments” as

follows:

Non-Complex Network Assets (Facilities, Vehicles,

Equipment, Land Improvements):

Service potential is enhanced (i.e. costs should be

capitalized as rehabilitation) when:

·

There is an increase in previously assessed output or service

capacity;

·

Operating costs are lowered;

·

Useful life is extended; or

·

The quality of output is improved (if applicable).

Complex Network Assets (Roads, Watermains, Wastewater

mains, Stormwater Mains):

Service potential is enhanced (i.e. costs should be

capitalized as rehabilitation) when:

·

There is an increase in previously assessed output or service

capacity. This may or may not increase the useful life of the applicable

assets.

To reiterate, the maintenance activities for complex network

assets – which are assets that form a network pattern – are those that maintain

the predetermined service potential of the applicable assets. This practice is

in place to ensure a maintenance activity (such as road-related pothole filling

or crack sealing) is recorded as maintenance, rather than recorded as

rehabilitation (i.e. capital). Even though pothole filling and crack sealing can

increase the remaining life of a road, these types of activities do not

increase the previously assessed service capacity.

Historical

Maintenance

Municipalities might first review historical maintenance

data as they begin to consider the appropriate level of planned maintenance to

undertake over a forecast period. The historical data may lead to a number of

question related to spending patterns, such as:

·

Is this the correct level of spending?

·

Should spending levels be higher or lower, and if so, on which

criteria should these decisions be based?

·

Where should the focus be for planned maintenance spending?

·

What has been the impact of historical maintenance on our assets?

If a municipality can assess the impact of current

maintenance activities on service levels (through asset condition and risk), it

can be determined whether the extent of those maintenance activities is

acceptable going forward over the forecast period, or if changes are required.

This will be discussed further in the next section.

The collection of historical maintenance data within the

asset register (see Chapter 3) can provide key data to assist in developing

future maintenance strategies. Areas of concern can be uncovered, providing a

basis for developing priorities. For example, assets may be identified that

required high maintenance historically, or the assets are experiencing

increasing maintenance costs over time, which may be supported by a declining

condition rating. It is incumbent upon municipalities to identify these types

of assets in order to be in the best position to direct resources and attention

where most needed. For example, a decision might be made to continue to

maintain the asset, which may require increasing the maintenance budget.

Conversely, a decision might be made to rehabilitate or replace the asset,

which could reduce future projected maintenance.

Maintenance Impact

on Assets

The decision to revise historical maintenance levels should

be made following an analysis of all lifecycle costs and expected levels of

service. For example, if an asset is not meeting expected levels of service,

the municipality will need to determine the lifecycle costs necessary to reach

those expected levels. These costs might include maintenance adjustments and,

potentially, other lifecycle costs (such as rehabilitation and replacement). Based

on a municipality’s maturity level, this can be done using a more high-level

(corporate) approach, a more intermediate asset type approach, or a more

detailed asset approach. Examples are provided in Table 5‑4 (below).

Table 5‑4

Sample Maintenance Solutions – Levels of Maturity

|

Maturity Level

|

Levels of Service Comments

|

Maintenance Impact

|

|

Basic

|

Assets as a whole are not meeting expected service levels

|

Increase all maintenance by 5% per year and monitor impact on

service levels annually

|

|

Intermediate

|

One particular asset type is not meeting expected service levels

|

Increase maintenance programs from $500,000 to $1.2 million over

10 years to provide expected levels of service (can be increases to existing

programs or new programs)

|

|

Advanced

|

One particular asset is not meeting expected service levels

|

Increase maintenance programs from $5,000 to $12,000 over 10 years

to provide a specific expected service level (can be increases to existing

programs or new programs)

|

What method is used to incorporate planned maintenance

solutions into the lifecycle management strategy?

Background

Municipalities engage in a number of approaches to determine

how much maintenance should be carried out in a given year. A simple approach

may be to base maintenance spending on prior years’ operating budgets, apply an

inflationary increase, and adjust for any necessary ad hoc adjustments for ‘out

of the ordinary’ or ‘new’ spending. Other municipalities will undertake a more

detailed approach, taking into account the condition of their assets, risk

levels, and desired levels of service to be provided.

Levels of Maturity

What method is used to incorporate planned maintenance

solutions into the lifecycle management strategy?

At the basic level of maturity, municipalities will

tend to incorporate planned maintenance solutions into the lifecycle management

strategy based on historical practices and may include subsequent ad hoc

adjustments. These municipalities will review and document historical

maintenance solutions that are in place. The impact of these practices on the

asset management process is assessed. Past practices are updated with any

high-level changes included in future maintenance plans. The associated impacts

of these changes is determined and considered for use in the budgeting process.

At the intermediate level of maturity, municipalities

incorporating planned maintenance into their lifecycle management strategy give

some consideration to asset condition, risk, and levels of service. Proposed

maintenance solutions are discussed and documented. Municipalities ensure the

proposed maintenance solutions will lead to some improvement in asset

condition, risk, and levels of service. The impact of these solutions on the

asset management process is assessed, with some consideration for the overall

impact on the long-term forecast and the assets’ remaining life.

At the advanced level of maturity, municipalities

incorporating planned maintenance into their lifecycle management strategy give

full consideration to asset condition, risk, and levels of service. Proposed

maintenance solutions are discussed and documented. Municipalities ensure the

proposed maintenance solutions fully take into account impacts on asset

condition, risk, and levels of service. The impact of these solutions on the

asset management process is assessed, with detailed consideration for the

overall impact on the long-term forecast and the assets’ remaining life.

Planned Maintenance

Strategy

This section introduces the concept of a “planned

maintenance strategy”, which identifies the role of planned maintenance in the

asset management planning process. Maintenance decisions should be made in consideration

with other lifecycle costs (i.e. rehabilitation and replacement), and be based

on factors such as:

·

Asset condition;

·

Asset risk; and

·

Expected levels of service.

Through this decision-making process the municipality will

need to answer:

Does maintenance provide an improvement in asset

condition, a mitigation of risk, and/or a movement towards expected levels of

service in an efficient and effective manner?

And,

Does maintenance defer other lifecycle costs to the point

where savings are projected?

These questions become more complicated when other lifecycle

costs are brought into the equation. Finding the optimal level of maintenance,

rehabilitation, and replacement lifecycle costs over a forecast period is the

definition of lifecycle optimization. Weighing the lifecycle costs against the

potential improvement in condition, mitigation of risk, and movement towards

expected service levels becomes the ultimate goal within the lifecycle

management strategy.

While planned maintenance should be integrated into

the asset management process, unplanned maintenance should be discussed

as well. Significant and dramatic increases in asset risk, even to the point of

asset failure, can represent a need for unplanned maintenance. While one of the

objectives of asset management planning is to minimize these events, they are

not completely avoidable. In the case of asset failure, municipalities will

need to assess whether the best strategy is to:

·

Perform maintenance work;

·

Rehabilitate;

·

Replace the asset;

·

Apply non-infrastructure solutions; or

·

Do nothing (i.e. allow the asset to continue to fail).

While considering the strategies above, municipalities need

to decide whether to base planned maintenance on historical trends or develop

new maintenance strategies that take risk and/or asset condition into account.

Either way, lifecycle costs should be quantified as part of the lifecycle

management strategy as well as the impact on the assets themselves. (i.e.

useful life, condition, risk, etc.).

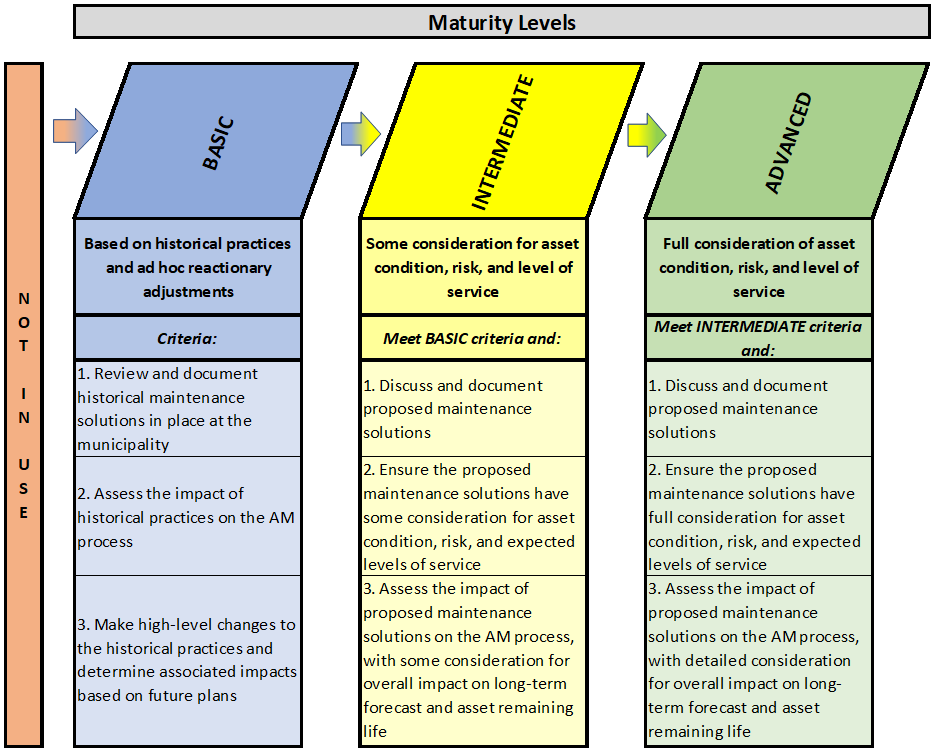

To what extent are planned rehabilitation solutions

incorporated into the lifecycle management strategy?

Background

Municipalities will approach planned rehabilitation

solutions in a number of ways. Some will base their plans on broad discussions

at the corporate level, whereas others will engage in more detailed discussions

with a focus on the asset type, or even at a detailed asset level.

Levels of Maturity

To what extent are planned rehabilitation solutions

incorporated into the lifecycle management strategy?

At the basic level of maturity, there will be some

high-level incorporation of planned rehabilitation solutions into the lifecycle

management strategy. Municipalities at the basic level of maturity engage in

broad discussions on current and/or potentially new planned rehabilitation

solutions. The impact of these solutions on the asset management process is

assessed at a corporate level. Finally, the planned rehabilitation analysis is

incorporated within the asset management plan calculations.

At the intermediate level of maturity, there will be

full incorporation of planned rehabilitation solutions into the lifecycle

management strategy at the asset type level. Municipalities engage in detailed

discussions on current and potential planned rehabilitation solutions to be

incorporated over the forecast period. The impact of these solutions on the

asset management process is assessed at the asset type level. Finally, the planned

rehabilitation analysis is incorporated within the asset management plan

calculations.

At the advanced level of maturity, there will be full

incorporation of planned rehabilitation solutions into the lifecycle management

strategy at a detailed asset level. Municipalities engage in detailed

discussions on current and potential planned rehabilitation solutions. The

impact of these solutions on the asset management process is assessed at a

detailed asset level. Finally, the planned rehabilitation analysis is

incorporated within the asset management plan calculations.

Rehabilitation vs.

Maintenance

Rehabilitation from an asset management perspective includes

significant repairs that, in many cases, extend asset life. Section 3150 of the

PSAB handbook provides an approach to identify rehabilitation (or

“betterments”) versus repairs and maintenance, as follows:

Non-Complex Network Assets (Facilities, Vehicles,

Equipment, Land Improvements):

Service potential is enhanced (i.e. costs should be

capitalized as rehabilitation) when:

·

There is an increase in previously assessed output or service

capacity;

·

Operating costs are lowered;

·

Useful life is extended; or

·

The quality of output is improved (if applicable).

Complex Network Assets (Roads, Watermains, Wastewater

mains, Storm Mains):

Service potential is enhanced (i.e. costs should be

capitalized as rehabilitation) when:

·

There is an increase in previously assessed output or service

capacity. This may or may not increase the useful life of the applicable

assets.

To reiterate, complex network assets – which are assets that

form a network pattern – rehabilitation activities increase the predetermined

service potential while maintenance activities simply maintain the

predetermined service potential of the applicable assets. This practice is in

place to ensure rehabilitation activities such as the lining of wastewater

mains are recorded as rehabilitation (i.e. capital). Conversely, maintenance

activities such as road-related pothole filling or crack sealing, should be

recorded as maintenance, rather than be identified as rehabilitation (i.e.

capital). Although pothole filling and crack sealing could increase the

remaining life of a road, these solutions do not increase the previously

assessed service capacity.

Historical

Rehabilitation

Municipalities might first review historical rehabilitation

data as they begin to consider the appropriate level of planned rehabilitation

to undertake over a forecast period. The historical data may lead to a number

of question related to spending patterns, such as:

·

Is this the correct level of spending?

·

Should spending levels be higher or lower, and if so, on which

criteria should these decisions be based?

·

Where should the focus be for planned rehabilitation spending?

·

What has been the impact of historical rehabilitation on our

assets?

If a municipality can assess the impact of current

rehabilitation practices on service levels (through asset condition and risk),

it can determine whether the extent of those rehabilitation practices is

acceptable going forward over the forecast period, or if changes are required.

This will be discussed further in Section 5.7.

As discussed in Section 5.5, the collection of historical

maintenance data within the asset register (see Chapter 3) can provide key data

to assist in developing future rehabilitation strategies. Areas of concern can

be uncovered, providing a basis for developing priorities. For example, assets

may be identified that required high maintenance historically, or the assets

are experiencing increasing maintenance costs over time, which may be supported

by a declining condition rating. It is incumbent upon municipalities to

identify these assets and be in the best position to direct resources and

attention where most needed. For example, the decision could be made to

continue to maintain the asset, which requires increasing the maintenance

budget. Conversely, the decision could be made to rehabilitate or replace the

asset, which could reduce future projected maintenance.

Rehabilitation

Impact on Assets

The decision to revise historical rehabilitation levels

should be made through an analysis of all lifecycle costs, based on expected

levels of service. For example, if an asset is not meeting expected levels of

service, the lifecycle costs needed to reach those levels must be determined.

This could include rehabilitation and, potentially, other lifecycle costs (such

as maintenance and replacement). Based on a municipality’s maturity level, this

can be done using a more high-level (corporate) approach, a more intermediate

asset type approach, or a more detailed asset approach. Examples are provided

in Table 5‑5 below:

Table 5‑5

Sample Rehabilitation Impacts

|

Maturity Level

|

Levels of Service Comments

|

Rehabilitation Impact

|

|

Basic

|

Assets as a whole are not meeting expected service levels

|

Increase all rehabilitation programs by 5% per year and monitor

impact on service levels annually for impact

|

|

Intermediate

|

One particular asset type is not meeting expected service levels

|

Increase rehabilitation from $1.0 million to $2.0 million over 10

years to provide expected levels of service (can be increases to existing

programs or new programs)

|

|

Advanced

|

One particular asset is not meeting expected service levels

|

Increase rehabilitation on specific asset over forecast period to

provide a specific expected service level (can be increases to existing

programs or new programs)

|

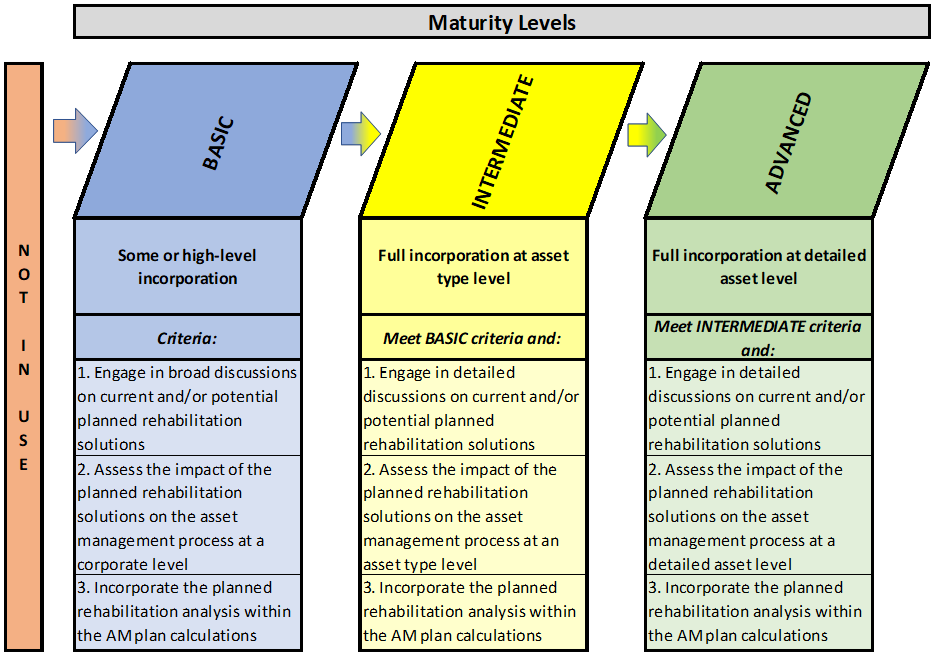

What method is used to incorporate planned rehabilitation

solutions into the lifecycle management strategy?

Background

Municipalities engage in a number of approaches to

incorporate planned rehabilitation solutions into the lifecycle management

strategy. A simple approach may be to base rehabilitation solutions on

historical practices, then incorporate any necessary ad hoc adjustments for

unexpected situations as they arise. Other municipalities may undertake a more

detailed approach, taking into account the condition of their assets, risk

levels, and desired levels of service to be provided.

Levels of Maturity

What method is used to incorporate planned rehabilitation

solutions into the lifecycle management strategy?

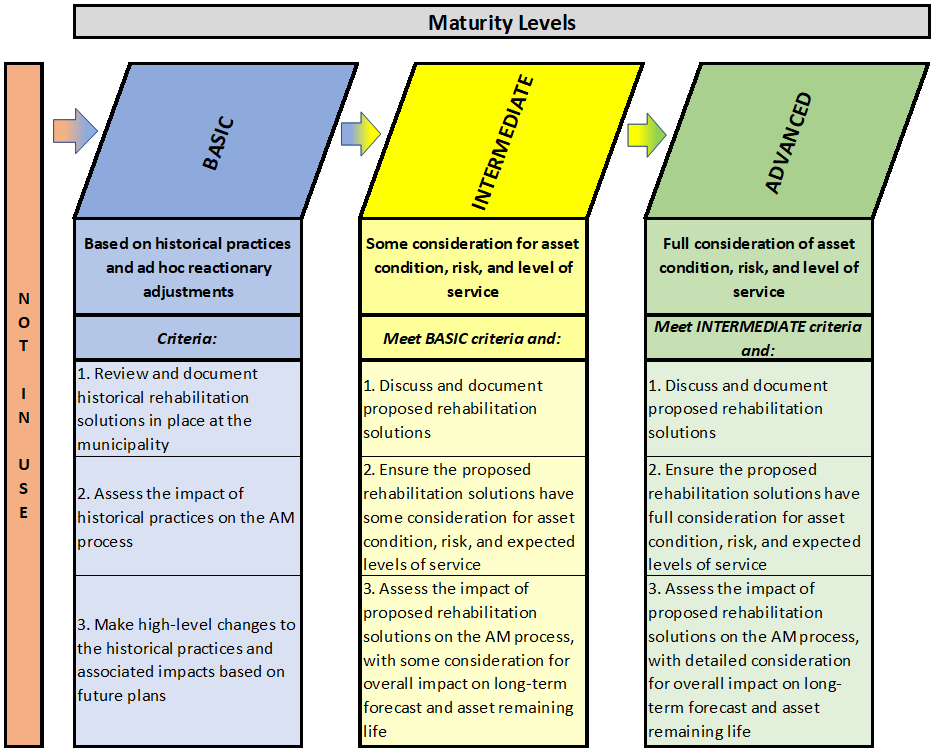

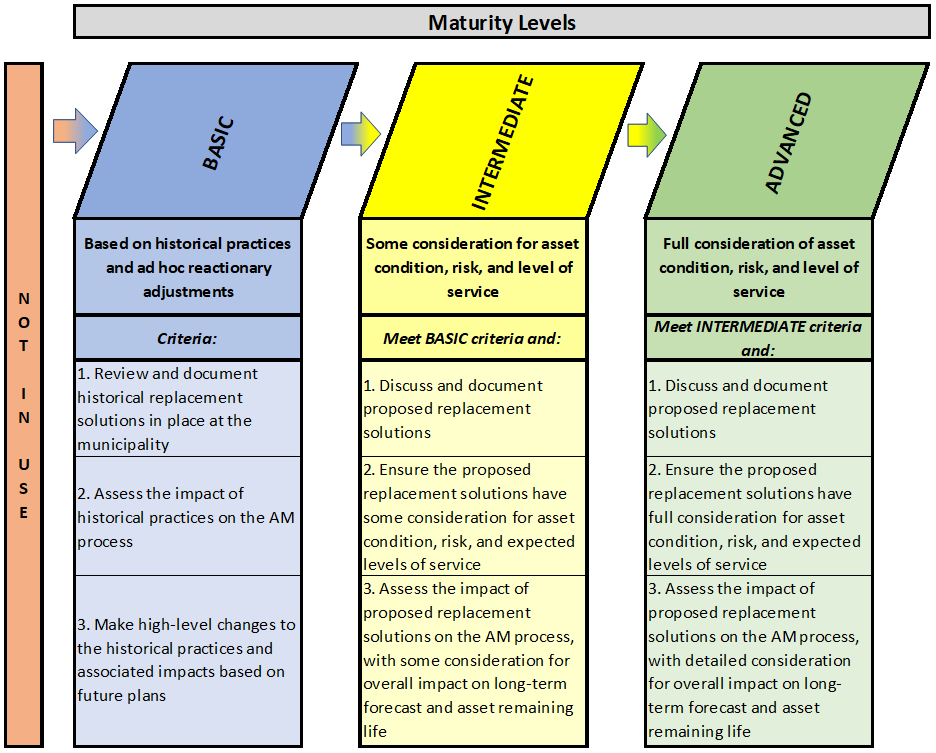

At the basic level of maturity, municipalities will

tend to incorporate planned rehabilitation solutions into the lifecycle management

strategy based on historical practices and may include subsequent ad hoc

reactionary adjustments. Municipalities will review and document historical

rehabilitation solutions that are in place. The impact of these practices on

the asset management process is assessed. Past practices are updated with any

high-level changes included in future rehabilitation plans. The associated

impacts of these changes is determined and considered for use in the budgeting

process.

At the intermediate level of maturity, municipalities

incorporating planned rehabilitation into their lifecycle management strategy

would give some consideration to asset condition, risk, and levels of service.

Proposed rehabilitation solutions are discussed at a staff level and

documented. Municipalities ensure the proposed rehabilitation solutions lead to

some improvement in asset condition, risk, and levels of service. The impact of

these solutions on the asset management process is assessed, with some

consideration for the overall impact on the long-term forecast and the assets’

remaining life.

At the advanced level of maturity, municipalities

incorporating planned rehabilitation into their lifecycle management strategy

give full consideration to asset condition, risk, and levels of service.

Proposed rehabilitation solutions are discussed at a staff level and

documented. Municipalities ensure the proposed rehabilitation solutions take

into account asset condition, risk, and levels of service. The impact of these

solutions on the asset management process is assessed, with detailed

consideration for the overall impact on the long-term forecast and the assets’

remaining life.

Planned

Rehabilitation Solutions - Approaches

Rehabilitation of certain assets can be appropriate when the

asset is not maintaining or moving towards expected service levels but is not

at a point in its lifecycle where replacement or maintenance is the optimal

course of action. To determine appropriate planned rehabilitation solutions for

the future, municipalities can follow different approaches. There are generally

three broad categories for rehabilitation:

1.

Top down

Under the top down approach, historical rehabilitation programs would be used

as a guide for future capital works. For example, municipalities may initiate “shave

and pave” programs for some of their roads at a budgeted annual cost and would

forecast continuing the program for a number of years. Similarly, a wastewater

main relining program may be undertaken over a number of years. Taking these

programs into account, municipalities would consider any adjustments to the

programs or whether to add new programs. The municipality should assess the

impact of these programs on the impacted assets’ remaining useful life,

replacement timelines, and the service being provided over time as the program

adjustments take effect. Example:

Figure 5‑2

Sample Rehabilitation Solutions – Top Down Approach

2.

Predictive modelling

The predictive modelling approach can be undertaken by municipal staff through

an analysis of a set of planned actions that account for predicted effects on

the assets and levels of service. This can be done at a broad level (by asset

type) or at a detailed level (by detailed asset). While this can be attempted

in spreadsheet format, asset management software would make this approach

easier to implement. See Chapter 9 for further discussions on software as an

asset management tool.

Figure 5‑3

Sample Rehabilitation Solutions – Predictive Modelling

Approach

3.

Bottom up

The bottom up approach is dependent on the identification of specific assets

that require attention (i.e. consider specific asset risk ratings, condition

ratings, and service levels). Assets identified would be scheduled for

rehabilitation, with the impacts on the assets’ remaining useful life and

replacement timelines once again considered. Complex predictive modelling can

assist with this process but is not required.

Figure 5‑4

Sample Rehabilitation Solutions – Bottom Up Approach

To put these categories in context of asset management

maturity:

Table 5‑6

Sample Planned Rehabilitation Approaches – Level of Maturity

|

Maturity Level

|

Categories

|

Approach

|

|

Basic

|

Top Down Approach at Corporate Level

|

High-Level Rehabilitation Analysis (Corporate Level)

Increase rehabilitation on all assets by 10%

|

|

Intermediate

|

Top Down or Predictive Modelling

at the Asset Type Level

|

Rehabilitation at the Asset Type Level

Increase rehabilitation on local roads by 10%

|

|

Advanced

|

Bottom Up or Predictive Modelling

at the Detailed Asset Level

|

Rehabilitation at the Detailed Asset Level

Increase rehabilitation on Smith St. by 10%

|

To what extent are planned replacement solutions

incorporated into the lifecycle management strategy?

Background

There are a number of ways that municipalities can approach

planned replacement solutions. Some may base their plans on broad discussions

at the corporate level, while others may engage in more detailed discussions

with a focus on the asset type, or even at a detailed asset level.

Levels of Maturity

To what extent are planned replacement solutions

incorporated into the lifecycle management strategy?

At the basic level of maturity, there will be some

high-level incorporation of planned replacement solutions into the lifecycle

management strategy. Municipalities engage in broad discussions on current and

potentially new planned replacement solutions to incorporate into the forecast.

The impact of these solutions on the asset management process is assessed at a

corporate level. Finally, the planned replacement analysis is incorporated

within the asset management plan calculations.

At the intermediate level of maturity, there will be

full incorporation of planned replacement solutions into the lifecycle

management strategy at the asset level. Municipalities engage in detailed

discussions on current and potential planned replacement solutions. The impact

of these solutions on the asset management process is assessed at an asset type

level. Finally, the planned replacement analysis is incorporated within the

asset management plan calculations.

At the advanced level of maturity, there will be full

incorporation of planned replacement solutions into the lifecycle management

strategy at a detailed asset level. Municipalities engage in detailed

discussions on current and potential planned replacement solutions. The impact

of these solutions on the asset management process is assessed at a detailed

asset level. Finally, the planned replacement analysis is incorporated within

the asset management plan calculations.

Replacement Program

Contrary to maintenance and rehabilitation identification,

the recognition of an asset being replaced is relatively straightforward. With

maintenance and rehabilitation, it will need to be determined whether the

predetermined service potential should be changed to classify a cost as

maintenance or rehabilitation (see Sections 5.5 and 5.6). Asset

replacement simply entails replacing one asset with another. The replacement

asset will either provide the same service potential or a completely different

service. Please refer to the discussion in Chapter 3 regarding the difference

between the reproduction cost and replacement cost of an asset.

Municipalities might first review historical replacement

levels undertaken over a forecast period. The historical data may lead to a

number of questions related to spending patterns, including:

·

Is this the correct level of spending?

·

Which criteria should drive decisions regarding spending levels?

·

Where should the focus be for planned replacement spending?

·

What has been the impact of historical replacement spending on

our assets?

If a municipality can assess the impact of current

replacement practices on service levels (through asset condition and risk), a

determination can be made regarding whether that level of replacement is

acceptable going forward over the forecast period, or if changes are required.

This analysis can also happen at the specific asset level, assessing

replacement needs on an asset-by-asset basis. This will be discussed further in

the next section.

As discussed in Sections 5.6 and 5.7, the collection of

historical maintenance data within the asset register (see Chapter 3) can

provide key insights to assist in the development of future replacement

strategies. Areas of concern can be uncovered, providing a basis for developing

priorities. For example, assets may be identified that required high

maintenance historically, or the assets are experiencing increasing maintenance

costs over time, which may be supported by a declining condition rating. It is

incumbent upon municipalities to identify such assets and be in the best

position to direct resources and attention where most needed. For example, the

decision could be made to continue to maintain the asset, which requires

increasing the maintenance budget. Conversely, the decision could be made to

rehabilitate or replace the asset, which could reduce future projected

maintenance.

Replacement Impact

on Assets

The decision to update historical replacement levels or

patterns to suit present and future needs should be based on an analysis of all

lifecycle costs and expected levels of service. For example, if a particular

asset is not meeting levels of service expectations, the lifecycle costs to be

incurred to move that asset towards providing expected service levels will need

to be determined. This could include replacement and potentially other

lifecycle costs (such as maintenance and rehabilitation). Based on the maturity

level of the municipality, this can be done using a more high-level (corporate)

approach, a more intermediate asset type approach, or a more detailed asset

approach. Table 5-7 provides examples of replacement impacts.

Table 5‑7

Sample Replacement Impacts – Level of Maturity

|

Maturity Level

|

Levels of Service Comments

|

Replacement Impact

|

|

Basic

|

Assets as a whole are not meeting expected service levels

|

Increase all replacement programs by 5% per year and monitor

impact on service levels annually

|

|

Intermediate

|

One particular asset type is not meeting expected service levels

|

Increase replacement program from $5.0 million to $9.0 million

over 10 years to provide an expected level of service

|

|

Advanced

|

One particular asset is not meeting expected service levels

|

Increase replacement on specific asset over forecast period to

provide a specific expected service level

|

What method is used to incorporate planned replacement

solutions into the lifecycle management strategy?

Background

Municipalities engage in a number of approaches to

incorporate planned replacement solutions into the lifecycle management

strategy. A simple approach may be to base replacement solutions on historical

practices, with any necessary ad hoc adjustments for unexpected situations as

they arise. Other municipalities may undertake a more detailed approach, taking

into account the condition of their assets, risk levels, and expected levels of

service to be provided.

Levels of Maturity

What method is used to incorporate planned replacement

solutions into the lifecycle management strategy?

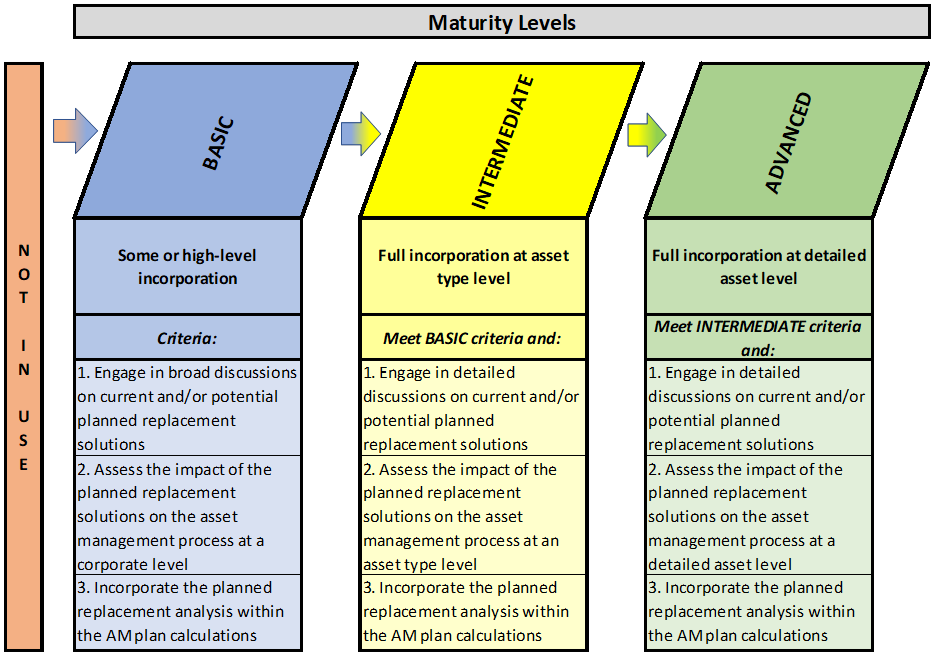

At the basic level of maturity, municipalities will

tend to incorporate planned replacement solutions into the lifecycle management

strategy based on historical practices and may include subsequent ad hoc

reactionary adjustments. Municipalities will review and document historical

replacement solutions that are in place. The impact of these practices on the

asset management process is assessed. Past practices are updated with any

high-level changes included in future replacement plans. The associated impacts

of these changes is determined and considered for use in the budgeting process.

At the intermediate level of maturity, municipalities

incorporating planned replacement into their lifecycle management strategy

would give some consideration to asset condition, risk, and levels of service.

Proposed replacement solutions are discussed at a staff level and documented. Municipalities

ensure the proposed replacement solutions lead to some improvement in asset

condition, risk, and levels of service. The impact of these solutions on the

asset management process is assessed, with some consideration for the overall

impact on the long-term forecast and the assets’ remaining life.

At the advanced level of maturity, municipalities

incorporating planned replacement into their lifecycle management strategy

would give full consideration to asset condition, risk, and levels of service.

Proposed replacement solutions are discussed at a staff level and documented. Municipalities

ensure the proposed replacement solutions have full consideration for asset

condition, risk, and levels of service. The impact of these solutions on the

asset management process is assessed, with detailed consideration for the

overall impact on the long-term forecast and the assets’ remaining life.

Planned Replacement

Solutions - Approaches

Replacement of assets can be appropriate when the asset is

not maintaining or moving towards expected service levels and has reached a

point in its lifecycle where rehabilitation or maintenance are no longer

optimal courses of action. In determining appropriate planned replacement

solutions for the future, municipalities can follow different approaches

(similar to the approaches identified for rehabilitation solutions above).

There are generally three broad categories:

1.

Top down

Under the top down approach, historical replacement programs would be used as a

guide for future capital works. For example, municipalities may initiate a road

surface replacement program for their roads at a budgeted annual cost, and

would forecast continuing the program for a number of years in the forecast.

Similarly, a wastewater main replacement program may be undertaken over a

number of years. Taking these programs into account, municipalities would

consider any adjustments to the programs or whether to add new programs. The

municipality should assess the impact of these programs on the impacted assets’

remaining useful life, replacement timelines, and the service being provided

over time as the program adjustments take effect. Example:

Figure 5‑5

Sample Replacement Solutions – Top Down Approach

2.

Predictive modelling

The predictive modelling approach can be undertaken by municipal staff through

an analysis of a set of planned actions that account for predicted effects on

the assets and levels of service. This can be done at a broad level (by asset

type) or at a detailed level (by detailed asset). While this can be attempted

in spreadsheet format, asset management software would make this approach

easier to implement. See Chapter 9 for further discussions on software as an

asset management tool.

Figure 5‑6

Sample Replacement Solutions – Predictive Modelling

Approach

3.

Bottom up

The bottom up approach is dependent on the identification of specific assets

that require attention (i.e. consider specific asset risk ratings, condition

ratings, and service levels). Assets identified would be scheduled for

replacement, with the impacts on the assets’ remaining useful life, and

replacement timelines once again considered. Complex predictive modelling can

assist with this process but is not required.

Figure 5‑7

Sample Replacement Solutions – Bottom Up Approach

To put these categories in context of asset management

maturity:

Table 5‑8

Sample Planned Replacement Solutions – Level of Maturity

|

Maturity Level

|

Categories

|

Approach

|

|

Basic

|

Top Down Approach at Corporate Level

|

High-Level Replacement Analysis (Corporate Level)

Increase replacement on all assets by 10%

|

|

Intermediate

|

Top Down or Predictive Modelling

at the Asset Type Level

|

Replacement at the Asset Type Level

Increase replacement on local roads by 10%

|

|

Advanced

|

Bottom Up or Predictive Modelling

at the Detailed Asset Level

|

Replacement at the Detailed Asset Level

Increase replacement on Smith St. by 10%

|

To what extent are growth and/or new service areas

incorporated into the lifecycle management strategy?

Background

Municipalities can approach the incorporation of growth

and/or new service areas in a number of ways. After compiling expansion needs

from existing reports and documentation, some will assess the impacts on

funding sources but only at the corporate level; some may take it a step

further by assessing impact on funding sources by service type area; whereas

others will go further still and assess impact on funding sources at the

detailed project level.

Levels of Maturity

To what extent are growth and/or new service areas

incorporated into the lifecycle management strategy?

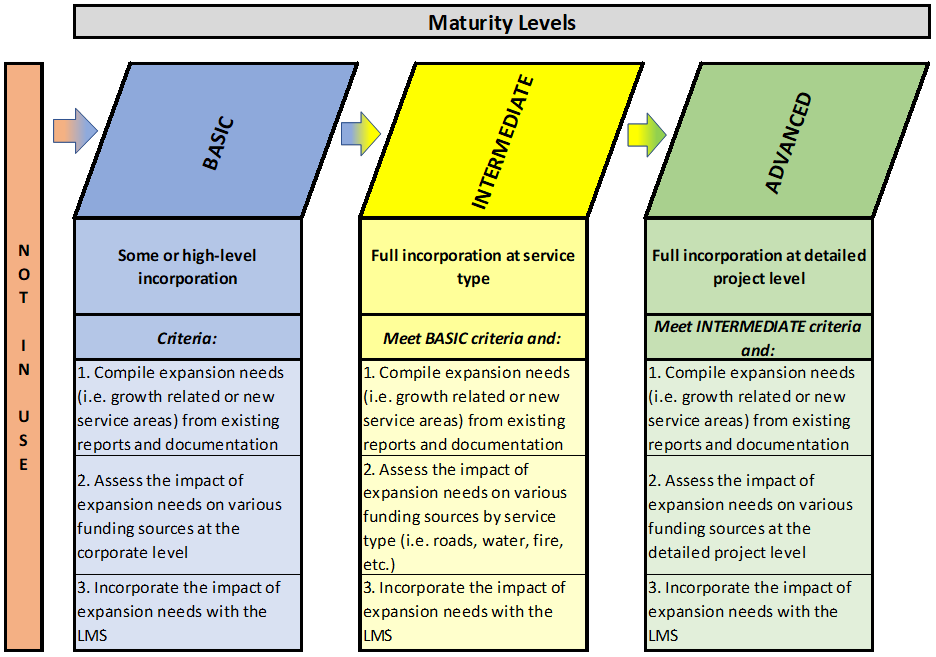

At the basic level of maturity, there will be some

incorporation or high-level incorporation of growth and/or new service areas

into the lifecycle management strategy. Municipalities compile expansion needs

(i.e. growth related or new service areas) from existing reports and

documentation. The impact of these expansion needs on various funding sources is

assessed, but generally at a high level only. The impact of the expansion needs

are incorporated into lifecycle management strategy.

At the intermediate level of maturity, there will be

full incorporation of growth and/or new service areas into the lifecycle

management strategy by service type. Municipalities compile expansion needs

(i.e. growth related or new service areas) from existing reports and

documentation. The impact of these expansion needs on various funding sources is

assessed by service type (i.e. roads, water, fire, etc.). The impact of the

expansion needs is incorporated into lifecycle management strategy.

At the advanced level of maturity, there will be full

incorporation of growth and/or new service areas into the lifecycle management

strategy at the detailed project or asset level. Municipalities compile

expansion needs (i.e. growth related or new service areas) from existing

reports and documentation. The impact of these expansion needs on various

funding sources is assessed at the detailed project level. The impact of the

expansion needs is incorporated into the lifecycle management strategy.

Assets Expansion

Previous sections have detailed elements of lifecycle

costing of existing assets within the context of the lifecycle management

strategy. This section explores how to handle new and/or expanded assets in

regards to upgrading, creating, purchasing, constructing, or receiving

contributed assets (with contributed assets discussed more fully later in this

chapter). As

municipalities grow, become more complex, and receive demands from residents,

expansion-related asset needs become a mechanism for allowing growth to occur

and to provide new or expanded services.

Sources of New and Upgraded Assets

The demand for new assets, or the requirement to upgrade

assets, can come from multiple sources, including:

1. Future Growth

Planning: A process which can identify the need for new or expanded assets

to meet increasing demands of providing existing services to an expanding population.

For example:

·

A requirement to increase the stormwater drainage capacity in a

high growth development area; or

·

The need to increase a two-lane road to a four-lane road due to

traffic congestion as a result of an increase in residents and housing in the

area.

2. Gaps in the

Levels of Service Provided: When comparing current service levels to

expected service levels,it may be determined that new or expanded assets are

necessary. For example:

·

The proposed level of service is to maintain parks every week.

Currently, parks are maintained every 2 weeks. To increase service levels, an

additional mower is needed.

3. Decision to

Provide a New Service: A municipality may decide that a new service is

required within the municipality (or a previously contracted service may become

a direct municipal service), resulting in the need for new or expanded assets

to support this service. For example:

·

A municipality may decide to run and operate their water and

wastewater systems, which was previously a contracted service. This requires

additional vehicles and equipment.

Determining Expansion Needs

Additional assets may be required as a result of the

following expansion-related circumstances:

1. Growth

Planning and New Services: Typically, these expansion needs are determined

outside of the asset management planning process. Municipalities will have

other various plans, policies, and strategies that deal with the concept of how

that particular municipality is to grow. This can include:

·

Strategic Plans;

·

Official Plans;

·

Secondary Plans;

·

Master Plans; and

·

Other (i.e. Capital Plans).

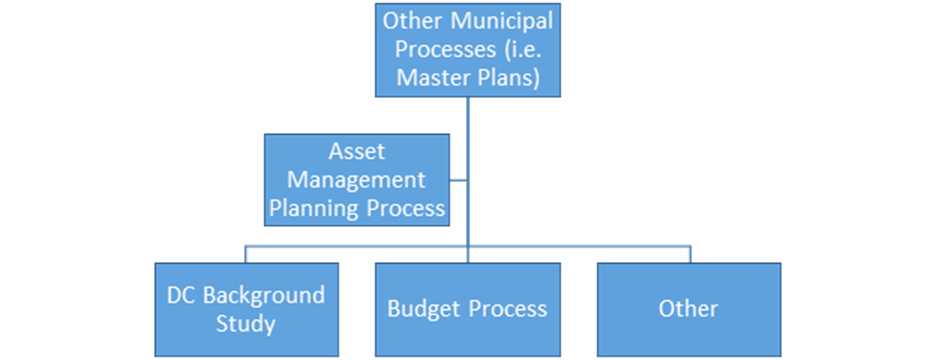

As illustrated in Figure 5-8 below, these

plans, policies, and strategies feed growth planning and new service needs into

the asset management process, as well as other processes, such as preparing a

Development Charge (DC) Background Study. It is, then, these other processes,

such as the DC Background Study, that can assist in determining allowable

funding sources within the Financing Strategy (see Chapter 6).

Figure 5‑8

Growth Planning and New Services Process

2.

Gaps in Levels of Service: These expansion needs can come from

the asset management planning process (such as the levels of service analysis –

see Chapter 4), or can be supported by other municipal processes such as

organizational reviews or efficiency/effectiveness reports.

To what extent are contributed assets incorporated into

the lifecycle management strategy?

Background

Municipalities can approach the incorporation of contributed

assets in a number of ways. After compiling details of anticipated contributed

assets from existing reports and documentation, some municipalities will assess

their impact on lifecycle management costs at the corporate level, whereas

others will focus on their impact on the lifecycle management costs by asset

type, or even at a detailed asset level.

Levels of Maturity

To what extent are contributed assets incorporated into

the lifecycle management strategy?

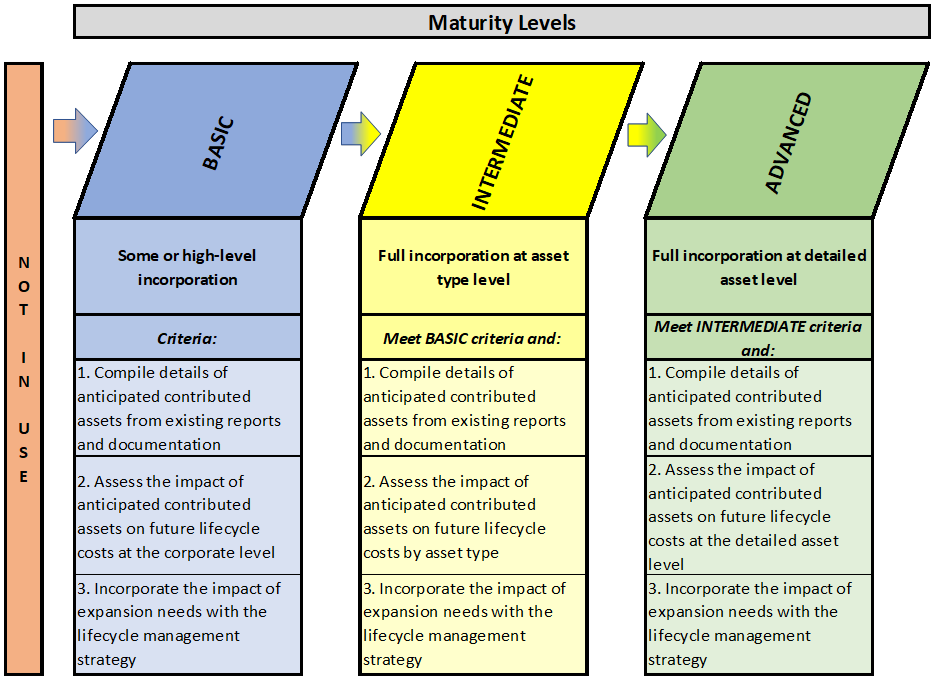

At the basic level of maturity, there will be some

incorporation or high-level incorporation of contributed assets into the

lifecycle management strategy. Municipalities at the basic level of maturity

will compile details of anticipated contributed assets from existing reports

and documentation. The impact on future lifecycle costs of these anticipated

contributed assets is assessed, but generally at the corporate level only. The

impact of the expansion needs is incorporated into the lifecycle management

strategy.

At the intermediate level of maturity, there will be

full incorporation of anticipated contributed assets into the lifecycle

management strategy at the asset type level. Municipalities at the intermediate

level of maturity will compile details of anticipated contributed assets from

existing reports and documentation. The impact of these expansion needs on

future lifecycle costs is assessed by asset type. The impact of the expansion

needs is incorporated into the lifecycle management strategy.

At the advanced level of maturity, there will be full

incorporation of anticipated contributed assets into the lifecycle management

strategy at the detailed asset level. Municipalities at the advanced level of

maturity will compile details of anticipated contributed assets from existing

reports and documentation. The impact of these expansion needs on future

lifecycle costs is assessed at the detailed asset level. The impact of the

expansion needs is incorporated into the lifecycle management strategy.

Contributed Assets

Contributed assets can include:

·

Assets assumed by a municipality, built by a developer (i.e.

completion of a subdivision where roads, stormwater, water, wastewater, parks,

etc. were included in the construction); and

·

Assets donated to a municipality (i.e. a community group), or a

community group agreeing to pay for a portion of an asset’s purchase or

rehabilitation.

The future lifecycle impact of contributed assets should be

accounted for within the asset management planning process. While the

municipality may not be responsible for the initial purchase or construction of

the asset, other lifecycle costs such as operations, maintenance, and future

rehabilitation or replacement will likely be the responsibility of the

municipality.

Each municipality should identify a consistent approach to accounting

for contributed assets from an asset management perspective. While, for

accounting purposes, these assets don’t have to be recorded until the date of

assumption, asset management consideration can occur before this event, if

desired. If the municipality has the ability to estimate the assets being

contributed (in terms of asset types and date of contribution), these estimates

can be used to start planning for future lifecycle costs within the lifecycle

management strategy (long-term forecast). The municipality’s approach to

determine the specific point in time to account for contributed assets in the

asset management process should be consistently applied, considering options

such as:

·

As soon as the municipality learns of the contributed assets;

·

The year (or year before) the contributed asset is anticipated to

be received/assumed; or

·

As soon as the contributed asset is recorded for accounting

purposes (typically date of assumption/receipt).

For this process to work, effective communication is needed

between municipal departments to ensure future contributed assets can be

identified in an appropriate manner, and at the right point in time.

How are risk assessments used within the lifecycle

management strategy?

Background

The previous sections of this chapter dealt with the

lifecycle cost categories that make up the lifecycle management strategy. This

section will explore how risk assessments are used to identify areas for focus

and priorities within the lifecycle management strategy. This will allow a

municipality to effectively mitigate risk while moving towards expected levels

of service from an asset management perspective.

During the management and maintenance of assets there is an

inherent risk associated with each activity. ISO 31000 – Risk management defines

risk as:

Acknowledging risks and managing them appropriately helps to

mitigate any implications associated with that risk, which enables municipal

staff and Council to make informed decisions around how to manage

infrastructure assets and their associated risks.

Levels of Maturity

How are risk assessments used within the lifecycle

management strategy?

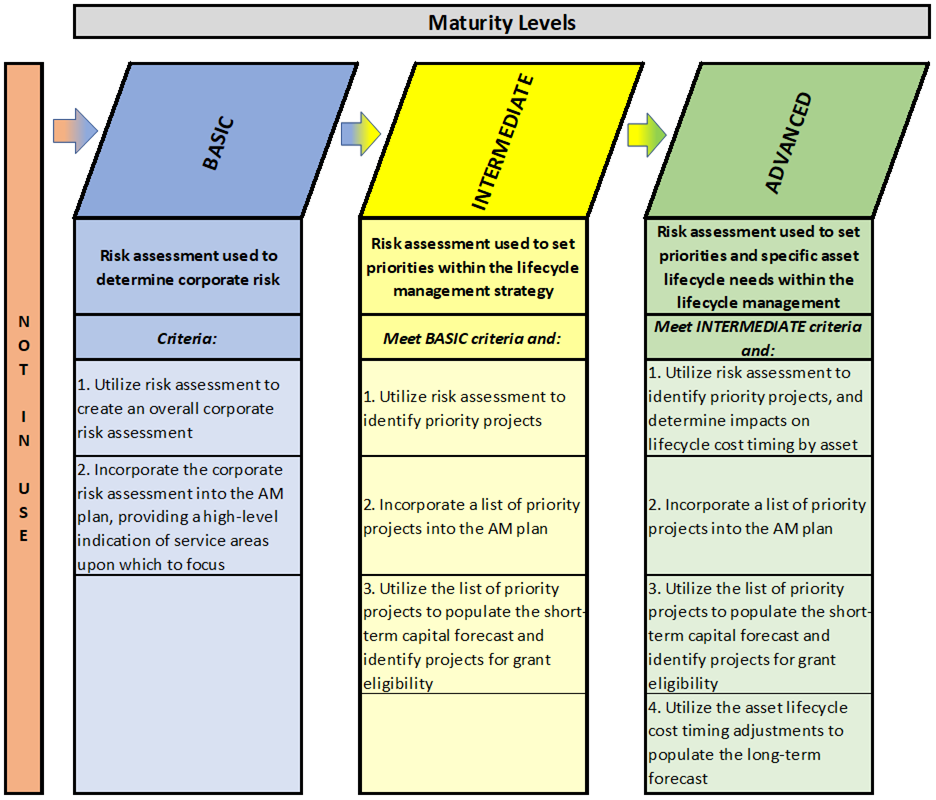

At the basic level of maturity, municipalities use

risk assessment to determine corporate risk by service area. The resulting

corporate risk assessment is incorporated into the asset management plan,

providing a high-level indication of service areas upon which to focus in the

lifecycle management strategy.

At the intermediate level of maturity, risk

assessments are used to set priorities within the lifecycle management

strategy. This is accomplished by utilizing risk assessment to identify

priority projects, and then incorporating the list of priority projects into

the lifecycle management strategy. The list of priority projects is utilized to

populate the short-term capital forecast and to form the basis for determining

grant eligibility.

At the advanced level of maturity, risk assessments

are used to set priorities, as well as specific asset lifecycle needs within

the lifecycle management strategy. Municipalities utilize risk assessments to

identify priority projects, and determine the related impacts on lifecycle cost

timing by specific asset. The list of priority projects is incorporated into

the lifecycle management strategy. The list of priority projects is also used

to populate the short-term to medium-term capital forecast and form the basis

for determining grant eligibility.

Risk Management

Approach

A risk management approach essentially defines what risk

management means to the organization.

For the purposes of asset management, there are two types of

risk:

1. Corporate

Risk: The corporate level risk assessment looks at risks that affect the

organization as a whole.

2. Asset

(Service) Risk: The activity level risk assessment looks at risks affecting

the management of a service and any associated infrastructure. This level of

risk assessment also considers corporate risk and is the level most relevant to

asset management.

One of the first steps in risk management is to understand

the organization and define the risk context. Factors that influence risk

management are identified through this process and a risk tolerance can be

defined.

Three steps can be followed for this process.

1. Conduct a review

that identifies internal and external factors that need to be considered when

managing risks corporately.

2. Determine the

organization’s risk tolerance, which can be expressed from the perspective of

the organization, or for different types of services/risk.

3. Develop an

overall risk management policy statement that is supported by staff and

Council.

In understanding the organization from a risk perspective, a

municipality should be able to describe the risk drivers affecting each service

area. As discussed in Chapter 3, this includes determining the probability of

assets failing as well as the consequence of assets failing, which results in

services “failing”. For services that utilize assets with a high probability

and/or consequence of failure, the minimization of risk can become a significant

objective of asset management planning. Please refer to Chapter 3 for details

on assessing asset risk.

Risk Management

Process

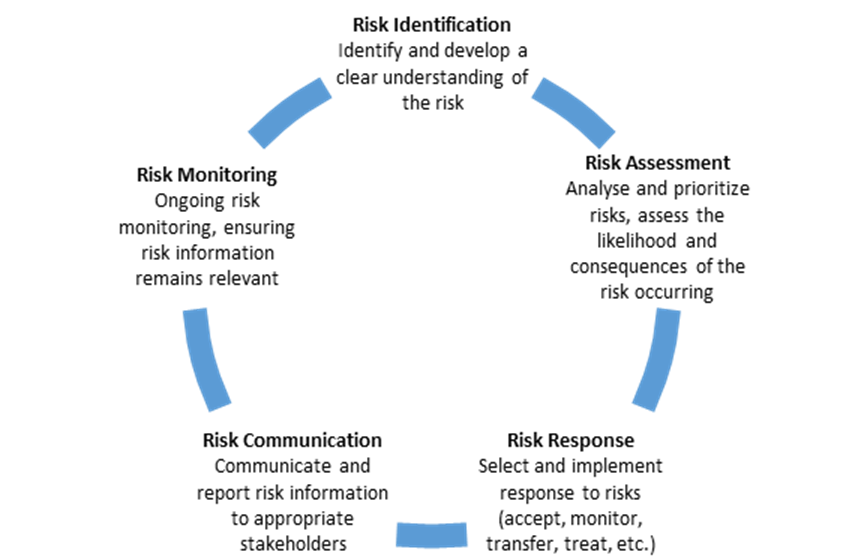

A risk management process is usually established as a

procedure and should be referred to in the asset management planning process

and be integrated into decision-making to assist in mitigating risk.

A risk management process is a series of inter-related steps

that guide the identification, assessment, response, communication, and

monitoring of risks. The risk management process outlined in the Treasury Board